PRINT AS PDF

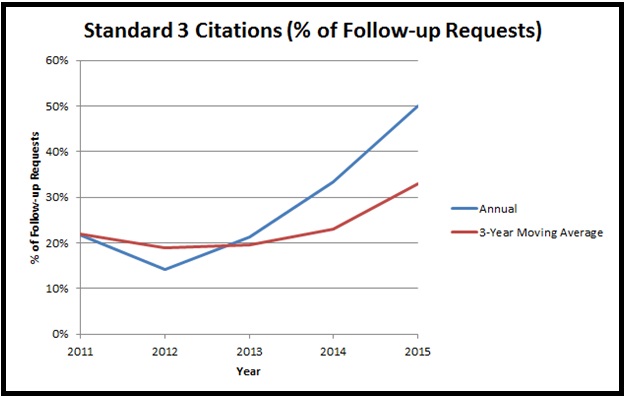

The last two Periodic Review Report (PRR) cycles witnessed a dramatic increase in the frequency of Standard 3 (Institutional Resources) being cited in requests for follow-up reports. During the 2014 PRR cycle, Standard 3 was cited in 32% of all follow-up requests. That ranked second, behind Standard 14 (Assessment of Student Learning). During the most recent PRR cycle, Standard 3 was cited in 50% of all follow-up requests, which was tied for highest with Standard 14. It is plausible that the PRR is becoming the Middle States Commission on Higher Education’s (MSCHE) tool for rigorously examining institutional finances.

As the U.S. economy has been growing at a moderate pace since the second quarter of 2009, challenging economic conditions cannot largely or fully explain the increasing focus on Standard 3. Instead, factors related to enrollment changes and their financial impact, likely play a role and perhaps an increasing one. A closer look at the citations reveals that there was a focus on financial projections/planning and the relationship between enrollment and finances during the 2015 PRR cycle.

The principal reasons behind the Standard 3 citations were as follows:

- Budget projections (multi-year or updated) or financial planning: 64% of Standard 3 citations

- Enrollment management plan/link to enrollment projections or trends: 45% of Standard 3 citations

- Ensure or strengthen financial viability/strengthen finances: 36% of Standard 3 citations

- Assessment of institutional resources/use of assessment results: 27% of Standard 3 citations

- Financial contingency plans (based on enrollment trends): 9% of Standard 3 citations

- Facilities master plan that is linked to the institution’s strategic plan: 9% of Standard 3 citations

In general, the Standard 3 citations suggest that an effective financial planning/budgeting process has the following attributes:

- Supports the institution’s mission and goals

- Is linked to the enrollment management plan/enrollment trends

- Is regularly assessed and assessment results are used to inform future planning

- Is sustainable

The first attribute can be evaluated from a regular reporting of outlays linked to an institution’s core activities and/or strategic goals/objectives. The second can be evaluated by measuring the impact of enrollment on institutional finances and providing financial assumptions related to the enrollment management plan. The third can be documented through a description of the assessment process, inclusion of assessment personnel/assessment office on any budget-related committees, and examples and evidence of how assessment results were used to inform the resource allocation process. The fourth can be determined through multi-year budget projections and an examination of the underlying assumptions (the credibility of the assumptions can be gleaned from a comparison between the assumptions and actual outcomes where modest differences suggest credible assumptions but frequent and large variances suggest flawed assumptions). Much of the data collected and analysis described above are things any effective institution should already be undertaking. They do not require new work. Instead, the lack of such data or analysis suggests existing flaws in controls related to planning and outcomes.

Finally, under the proposed changes to MSCHE’s accreditation cycle, the Mid-Point Peer Review may play a similar role. Based on MSCHE’s Special Edition Newsletter of November 2015, that process will focus on an institution’s “on-going improvement efforts” and its overall “health,” drawing upon data related to its prior self-study findings and updates to annual institutional updates, which include enrollment and retention rate data. The new cycle could raise the importance of an institution’s enrollment management plan (whether the plan is realistic e.g., outcomes vs. plan) given the relationship between enrollment and finances.